This article is a constructive blueprint to elevate India’s regional aviation landscape. We acknowledge and commend the significant strides already made under various central and state government initiatives, especially the UDAN scheme and the likes providing intra-state connectivity, which have brought the dream of “Ude Desh Ka Aam Nagrik” closer to reality. However, to fully unlock the potential of intra-national air mobility and bring it on par with countries that boast robust regional air networks, it is essential to address the residual gaps that continue to hinder sustainable growth.

In the first two sections, we provide a status overview of India’s regional connectivity and identify the bottlenecks—structural, operational, and economic—that limit its full-scale success. In the third section, we propose practical solutions and scalable strategies to bridge these gaps. The fourth section outlines policy interventions and funding frameworks that can accelerate progress. Lastly we close with our final thought “Let’s Reimagine Regional, Not Just Connect It”.

1. The Promise and the Paradox: A Snapshot of Regional Aviation in India

India, the world’s third-largest domestic aviation market, remains largely underserved when it comes to regional connectivity. Despite over 450 airstrips and airports dotting the country, less than 100 are currently operational with scheduled commercial services. This is a paradox. While Tier-1 cities are increasingly saturated with high-frequency routes and competition, the vast hinterland — with its growing economic aspirations and demand for faster connectivity — remains disconnected.

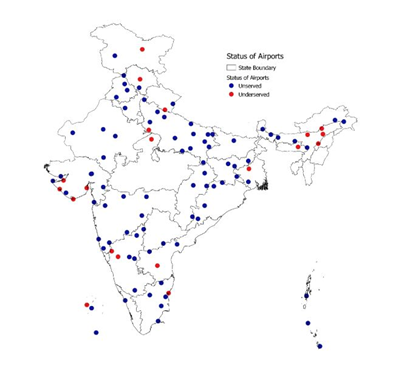

Fig 1. Representation of Unserved & Underserved Airports in India

(Image credits: ISB)

The Numbers Speak

According to the Airports Authority of India (AAI), nearly 275 million people live in Tier-2 and Tier-3 cities with limited or no direct air access. While the UDAN scheme (Ude Desh ka Aam Naagrik) launched in 2016 aimed to bridge this gap, progress has been mixed. Of the total number of routes awarded under various UDAN rounds, only about 52.3% were fully operational as of 2024, many with poor load factors or inconsistent service continuity.

Similarly, take for example, the case of Madhya Pradesh. The state’s MP Tourism Deptt launched it’s Intra State Air Taxi Connectivity under the name “PM Shri Paryatan Vayu Sewa” with much fanfare. The scheme launched on 13th June 2024, connected 08 districts of MP viz Bhopal, Jabalpur, Rewa, Singrauli, Gwalior, Indore, Khajuraho and Satna. While the demand remains high, the scheme struggles with low aircraft and trained manpower availability, thereby shelving several of the initial destinations from it’s schedule.

UDAN STATS AS ON 31.05.2025:

Total number of RCS Airports operationalized as on 31-05-2025: 92

(This 92 includes 20 Underserved and 72 Unserved airports)

Total Routes Commenced under various UDAN schemes: 635 (Breakdown below)

| UDAN Scheme (Phases) |

Routes Commenced (In Numbers) |

Route Types | No. Of Routes |

| UDAN 1.0 UDAN 2.0 UDAN 3.0 UDAN 4.0 UDAN 4.1 UDAN 4.2 UDAN 4.3 UDAN 5.0 UDAN 5.1 UDAN 5.2 UDAN 5.3 |

56 156 167 54 46 30 10 70 16 02 28 |

Tourism Routes DoNER Routes Helicopter Routes Seaplane Routes |

53 6 70 02 |

| Total | 635 |

Table 1: UDAN Stats as on 31.05.2025

A Few Missed Opportunities

From textile hubs in Tiruppur to tech clusters in Indore and tourism hotspots like Gwalior or Puri — several high-potential regions still depend on cumbersome road or rail journeys. Meanwhile, operators struggle with structural bottlenecks: poor airport infrastructure, aircraft acquisition hurdles, high cost per available seat kilometre (CASK), and limited maintenance and crew support in outlying regions.

Global Lessons, Local Challenges

Countries like Brazil, Canada, and Indonesia, with similarly dispersed geographies, have fostered thriving regional networks using small aircraft, intermodal hubs, and community-supported routes. India has yet to fully unlock such potential, despite having the demographic and economic logic to support it.

Case in Point: Brazil’s Azul Airlines operates nearly 900 daily flights across more than 150 domestic destinations, with ATRs and Embraers forming the backbone of its regional strategy. This model, tweaked for Indian conditions, can guide the next phase of regional aviation.

2. Why Previous Attempts Have Struggled — And What We Can Learn

Despite policy support, financial incentives, and growing regional demand, regional aviation in India has struggled to gain altitude. A deeper look reveals that most failures are rooted not in ambition, but in flawed execution and structural misalignments.

2.1. Weak Business Models and Lack of Scale

Many regional carriers launched under UDAN were undercapitalized, lacked fleet commonality, and operated with sub-optimal aircraft types. In their rush to capitalize on subsidies, several overlooked route viability and scalability.

Example: Airlines like the erstwhile Air Deccan were awarded 34 routes in the first round of bidding for the scheme and began operations under UDAN in December 2017. However it ceased operations, citing unsustainable cost structures and operational inefficiencies. Similarly Zoom Air and Air Odisha showed much enthusiasm but their bids got rejected in the third round of UDAN due to concerns of their financial stability and ability to undertake safe operations.

Unlike global peers, Indian regional players often operated with fewer than 5 aircraft — too small to spread fixed costs and to exploit flexibility. To amplify a bit, fixed costs like CAMO, AOC compliance, crew training, and spares inventory get better distributed across a larger fleet. Similarly larger fleet size gives more leeway in aircraft rotation, maintenance scheduling, crew management, and charter/on-demand ops. With just a few aircraft, even one AOG event or one unavailable pilot can disrupt the whole network.

2.2. Infrastructure Deficits at Regional Airports

While UDAN aimed to revive unused airports, many lacked basic operational facilities: night landing capabilities, instrument landing systems (ILS), airstrip periphery walls, 24×7 police presence and qualified technical manpower.

Stat: As of mid-2023, over 35 UDAN airportsremained non-operational due to inadequate infrastructure or absence of a viable operator.

Such bottlenecks not only deter operators but also undermines schedule reliability, passenger confidence, and operational continuity. Jalgaon Airport for example has two FTO’s namely Skynex Aero and FlyOla. Both were allotted space and the two commenced operations a couple of years ago. However the glitch of not providing electricity to the FTO’s hangars by the State/AAI remained and the two continued to run their 24×7 operations through massive diesel generators thereby not only polluting the atmosphere but also adding to their operating overheads.

| List of RCS Airports operationalized as on 31-05-2025 (Total 92. This includes 20 Underserved and 72 Unserved airports) |

||||

| S No. | State | Airport | Owner | Date of Operationalisation |

| 1. | Andhra Pradesh | Kadapa (Underserved) | AAI | 27‐April‐2017 |

| 2. | Kurnool (Unserved) | AP Airports Dev. Corp. Ltd |

28‐march 2021 | |

| 3. | Arunachal Pradesh | Tezu (Unserved) | AAI | 15.August.2021 |

| 4. | Passighat (Unserved) | IAF (CE‐SG) | 24‐May 2021 | |

| 5. | Hollongi (Unserved) | AAI | 15‐Jan‐2023 | |

| 6. | Assam | Jorhat (Underserved) | IAF(CE‐AAI) | 1‐Aug‐2018 |

| 7. | Lilabari (Underserved) | AAI | 15‐Jan‐2019 | |

| 8. | Tezpur (Underserved) | IAF(CE‐AAI) | 26‐April‐2018 | |

| 9. | Rupsi (Unserved) | AAI | 8‐May 2021 | |

| 10. | Bihar | Darbhanga (Unserved) | IAF(CE‐AAI) | 08‐Nov‐2020 |

| 11. | Chhattisgarh | Jagdalpur (Unserved) | State Govt. | 14‐June‐2018 |

| 12. | Bilaspur (Unserved) | State Govt. | 1‐March‐2021 | |

| 13. | Ambikapur (Unserved) | State Govt. | 19‐Dec‐2024 | |

| 14. | Daman & Diu | Diu (Underserved) | AAI | 24‐Feb‐2018 |

| 15. | Gujarat | Bhavnagar (Underserved) | AAI | 1‐May‐2018 |

| 16. | Jamnagar (Underserved) | IAF (CE‐AAI) | 17‐Feb‐2018 | |

| 17. | Kandla (Unserved) | AAI | 1‐July‐2017 | |

| 18. | Keshod (Unserved) | AAI | 16‐Apr‐2022 | |

| 19. | Mundra (Unserved) | Private | 17‐Feb‐2018 | |

| 20. | Porbandar (Underserved) | AAI | 10‐July‐2017 | |

| 21. | Statue of Unity (W) (Unserved) | State Govt. | 31‐Oct‐2020 | |

| 22. | Sabarmati River Front (W) (Unserved) | State Govt. | 31‐Oct‐2020 | |

| 23. | Haryana | Hissar (Unserved) | State Govt. | 14‐Jan‐2021 |

| 24. | Himachal Pradesh | Shimla (Unserved) | AAI | 27‐April‐2017 |

| 25. | Kullu (Underserved) | AAI | 13‐May‐2019 | |

| 26. | Mandi – Heliport (Unserved) | State Govt. | 09‐Dec‐2021 | |

| 27. | Rampur – Heliport (Unserved) | State Govt. | 14‐Dec‐2021 | |

| 28. | Jharkhand | Deoghar (Unserved) | AAI‐Jharkhand (JV) | 12‐July‐2022 |

| 29. | Jamshedpur (Unserved) | TATA Steel Ltd. | 31‐Jan‐2023 | |

| 30. | Karnataka | Belgaum (Underserved) | AAI | 1‐May‐2019 |

| 31. | Hubli (Underserved) | AAI | 14‐May‐2018 | |

| 32. | Mysore (Unserved) | AAI | 2‐Sep‐2017 | |

| 33. | Vidyanagar (Unserved) | Private | 21‐Sep‐2017 | |

| 34. | Kalaburgi (Gulbarga) (Unserved) | AAI | 22‐Nov‐2019 | |

| 35. | Bidar (Unserved) | IAF(CE‐SG) | 07‐Feb‐2020 | |

| 36. | Shivamogga (Unserved) | SG | 21‐Nov‐2023 | |

| 37. | Kerala | Kannur (Unserved) | Private (KIAL) | 25‐Jan‐2019 |

| 38. | Lakshadweep | Agatti (Underserved) | AAI | 18‐April‐2024 |

| 39. | Madhya Pradesh | Gwalior (Underserved) | IAF (CE‐AAI) | 31‐May‐2017 |

| 40. | Rewa (Unserved) | State Govt. | 25‐Nov‐2024 | |

| 41. | Datia (Unserved) | State Govt. | 31‐May‐2025 | |

| 42. | Maharashtra | Gondia (Unserved) | AAI | 13‐March‐2022 |

| 43. | Jalgaon (Unserved) | AAI | 23‐Dec‐2017 | |

| 44. | Kolhapur (Unserved) | AAI | 8‐April‐2018 | |

| 45. | Nanded (Unserved) | Reliance | 27‐April‐2017 | |

| 46. | Ozar (Nasik) (Unserved) | HAL | 23‐Dec‐2017 | |

| 47. | Sindhudurg (Unserved) | IRB Infra | 9‐October ‐2021 | |

| 48. | Amravati (Unserved) | MADC | 16‐April‐2025 | |

| 49. | Manipur |

Jiribam Heliport (Unserved) | State Govt. | 13.March.2024 |

| 50. | Tamenglong Heliport (Unserved) | State Govt. | 13.March.2024 | |

| 51. | Meghalaya | Shillong (Underserved) | AAI | 26‐April‐2018 |

| 52. | Nagaland | Dimapur (Underserved) | AAI | 07‐Dec‐2019 |

| 53. | Odisha | Jharsuguda (Unserved) | AAI | 22‐Sep‐2018 |

| 54. | Jeypore (Unserved) | State Govt. | 03‐Aug‐2022 | |

| 55. | Rourkela (Unserved) | SAIL | 07‐Jan‐2023 | |

| 56. | Utkela (Unserved) | State Govt. | 31‐Aug‐2023 | |

| 57. | Pondicherry (UT) | Pondicherry (Underserved) | AAI | 16‐Aug‐2017 |

| 58. | Punjab | Adampur (Unserved) | IAF(CE‐AAI) | 1‐May‐2018 |

| 59. | Bhatinda (Unserved) | IAF(CE‐AAI) | 27‐April‐2017 | |

| 60. | Ludhiana (Unserved) | AAI | 2‐Sep‐2017 | |

| 61. | Pathankot (Unserved) | IAF(CE‐AAI) | 5‐April‐2018 | |

| 62. | Rajasthan | Bikaner (Unserved) | IAF(CE‐AAI) | 26‐Sep‐2017 |

| 63. | Jaisalmer (Unserved) | IAF(CE‐AAI) | 29‐Oct‐2017 | |

| 64. | Kishangarh (Unserved) | AAI | 8‐Oct‐2018 | |

| 65. | Sikkim | Pakyong (Unserved) | AAI | 4‐Oct‐2018 |

| 66. | Tamil Nadu | Salem (Unserved) | AAI | 25‐Mar‐2018 |

| 67. | Uttar Pradesh | Agra (Underserved) | IAF(CE‐AAI) | 8‐Dec‐2017 |

| 68. | Aligarh (Unserved) | State Govt. | 11‐March‐2024 | |

| 69. | Azamgarh (Unserved) | State Govt. | 11‐March‐2024 | |

| 70. | Bareilly (Unserved) | IAF(CE‐AAI) | 08‐Mar‐2021 | |

| 71. | Chitrakoot (Unserved) | State Govt. | 12‐March‐2024 | |

| 72. | Moradabad (Unserved) | AAI | 10‐August‐2024 | |

| 73. | Prayagraj (Underserved) | IAF(CE‐AAI) | 14‐June‐2018 | |

| 74. | Kanpur (Chakeri) (Unserved) | IAF(CE‐AAI) | 3‐July‐2018 | |

| 75. | Hindon (Unserved) | IAF(CE‐AAI) | 11‐Oct‐2019 | |

| 76. | Shravasti (Unserved) | State Govt. | 12‐March‐2024 | |

| 77. | Kushinagar (Unserved) | AAI | 26‐Nov‐2021 | |

| 78. | Uttarakhand | Pantnagar (Underserved) | AAI | 4‐Jan‐2019 |

| 79. | Pithoragarh (Unserved) | State Govt. | 17‐Jan‐2019 | |

| 80. | Sahastradhara ‐ Heliport (Unserved) | State Govt. | 08‐Feb‐2020 | |

| 81. | Chinyalisaur –Heliport (Unserved) | State Govt. | 08‐Feb‐2020 | |

| 82. | Gaucher –Heliport(Unserved) | State Govt. | 08‐Feb‐2020 | |

| 83. | New Tehri –Heliport(Unserved) | State Govt. | 29‐July‐2020 | |

| 84. | Srinagar –Heliport(Unserved) | State Govt. | 29‐July‐2020 | |

| 85. | Haldwani – Heliport(Unserved) | State Govt. | 8‐Oct‐2021 | |

| 86. | Almora – Heliport (Unserved) | Army | 26‐Aug‐2022 | |

| 87. | Champawat-Heliport(Unserved) | State Govt. | 22‐Feb‐2024 | |

| 88. | Munsyari – Heliport (Unserved) | State Govt. | 22‐Feb‐2024 | |

| 89. | Nainital – Heliport (Unserved) | State Govt. | 12‐Mar‐2025 | |

| 90. | Bageshwar – Heliport (Unserved) | State Govt. | 12‐Mar‐2025 | |

| 91. | West Bengal | Cooch Behar (Unserved) | AAI | 21‐Feb‐2023 |

| 92. | Durgapur (Underserved) | Private | 25‐June‐2019 | |

Table 2 – List of RCS Airports as on 31.05.2025.

The above list can help aviation enthusiasts, investors and operators alike to exploit the full potential of these airstrips and identify the unserved ones and associate in their upgradation and connectivity on a win-win basis

2.3. Inappropriate Aircraft Choice

Several carriers opted for ageing or ill-suited aircraft with high maintenance needs and poor dispatch reliability. With little local MRO support and spares supply, these aircraft became financial sinkholes.

Learning from Canada: In contrast, Canadian operators such as Porter Airlines have embraced modern turboprops (e.g., De Havilland Dash 8 Q400s), which offer superior economics and are backed by reliable OEM support.

India needs to adopt a similar approach: standardized, fuel-efficient aircraft with OEM and MRO infrastructure in place.

2.4. Over-reliance on Subsidies

UDAN was never meant to replace commercial viability. Unfortunately, several operators built their models around Viability Gap Funding (VGF) as the primary revenue stream. Once subsidies ended or reimbursements got delayed, sustainability nosedived.

Critical Insight: In business parlance, it’s the first 3 to 5 years that are critical. Once a company crosses this threshold, it soars. Subsidies should incentivize entry — not become a permanent crutch. Global examples suggest that regional aviation thrives only when supported by demand-side fundamentals, not perpetual subsidies.

2.5. Regulatory & Licensing Delays

From airport licensing to NSOP certifications, operators often face prolonged regulatory wait times. This despite the government’s digitization initiative viz the Egca having automated processes resolving much of the inadvertent delays due over dependence on paperwork. Additionally, the lack of clarity around pilot licensing equivalency, non-provision of rent free gestation periods to put up infra like hangars and building tarmacs and cross-utilization of manpower further complicates operations. Just to gauge the impact, let’s take the example of AME Licenses. There continues to be a hue and cry w.r.t shortage of AME’s in the General Aviation. To overcome the issue, DGCA started doling out CAR 147 approvals to organizations after some due diligence. A study if conducted on whether these organizations have effectively utilized their enhanced capability to overcome the shortage of AME’s or simply using it as a medal to flaunt, will reveal the actual output vis a vis the efforts put in.

2.6. Poor Marketing and Awareness

In many Tier-3 towns, people are unaware of the availability or affordability of regional flights. Without aggressive outreach, even scheduled routes report dismal load factors.

Observation: Operators rarely invest in localized digital campaigns, community engagement, or travel agent partnerships — missing out on critical demand aggregation opportunities.

In Summary:

India’s regional aviation model needs to shift from subsidy-dependence to sustainable, scale-driven operations backed by infrastructure readiness, right-sized aircraft, efficient cost management, and better community integration.

3. A Blueprint for Scalable, Profitable Tier-2/Tier-3 Connectivity

Reimagining regional aviation in India requires a systemic redesign — not just incremental tweaks. The blueprint below outlines a framework that aligns economic viability, infrastructure development, and regulatory innovation to build a sustainable ecosystem for Tier-2 and Tier-3 air connectivity.

3.1. Fleet Strategy: Right-Sized, Modern, Supported

Aircraft selection must shift from opportunistic acquisitions to strategic ones. Operators should adopt a fleet of 18–70 seaters, with modern turboprops or light regional jets that offer:

- Low operating costs (less than ₹6,000 per block hour)

- High dispatch reliability

- Short takeoff and landing (STOL) capability to utilize many 5000 ft runways scattered around India.

- OEM-backed spares and MRO support in India

Best Practice Example:

Wheels Up (USA) and Skyward Express (Kenya) both operate cost-effective regional fleets (Beechcraft 1900D, Dash 8, Cessna Caravan) that serve hard-to-reach destinations with profitability due to asset-light structures and strong vendor support.

Recommendation:

- Aircraft Recommended: ATR 42-600 (Pax: 48), Viking Twin Otter, DHC-6 Series 400 (Pax: 18 to 19), Dash 8 Q100/200/300 series (Pax: 37 to 50), Embraer’s E175 (Pax: 70). More suitable ones can be explored.

- Indian NSOPs, UDAN and other regional operators should explore co-leasing arrangements and OEM support pools to mitigate capital risk and improve turnaround times. This becomes all the more easier with the Indian Parliament approving the “Protection of Interest in Aircraft Objects Bill” on 03rd April 2025. This is bound to help reduce risks and costs for aircraft lessors thereby encouraging them to lease aircraft to scheduled and Non-scheduled airlines in India on comparatively flexible terms.

3.2. Airport Optimization: The 40:20:40 Rule

Not every town needs a full-fledged airport. Instead, implement a “40:20:40 Airport Framework”:

- 40%: Tier-2 airports with night ops, ILS, and security capabilities

- 20%: High-potential Tier-3 airstrips upgraded with modular terminal tech (₹15–25 crore capex) and extended runway lengths beyond 5000 ft.

- 40%: Heliports and STOL strips with DGCA-approved Final Approach & Take Off (FATO) zones for last-mile air taxis

ROI Insight: Small airport projects (<₹50 crore) yield upto 3 times the ROI (3x ROI) in 5–7 years when matched with tourism or industrial clusters like for example Deoghar, Gondia, Kandla, Khajuraho to name a few. The recently connected Singrauli airstrip in MP is another example of buzzing demand for air travel due to it being a hub for coal mining and power generation.

3.3. Air Route Planning via Data & Demand Heatmaps

Move away from politically mapped routes and use AI-based demand mapping:

- Analyze rail/road density and travel time > 7 hrs

- Identify clusters with > 1 lakh monthly intercity movement

- Leverage GDS, IRCTC, Ola/Uber ride data to discover underserved city pairs

Insight: Demand between Madurai–Tirupati, Patna–Ranchi, Raipur–Nagpur, or Jaisalmer–Bikaner often exceeds 15,000 monthly passengers via indirect modes — enough for 12–15 weekly rotations on a 18-seater.

3.4. Public–Private Partnerships (PPP) for Operator Clusters

Just like the Govt adopted the PPP model for accelerating the construction of many a highways across the country, the state governments should be encouraged to co-invest in Operator Collectives, where 2–4 NSOPs pool fleets and back-end ops under a joint holding entity:

- Shared MRO base

- Centralized CAMO/QMS team

- State co-funding of aircraft acquisition (like Viability Gap Funding 2.0)

Case Study: The Papua New Guinea Airlines Alliance, supported by the government and local investors, runs a regional network with 4 carriers using a shared booking system and common technical backend.

3.5. Digital-First Experience for Tier-2 Travelers

Bring mobile-first UX, dynamic pricing, real-time tracking, and WhatsApp-based boarding passes to regional routes. Integrate with:

- UPI-enabled ticketing

- DigiYatra

- Regional travel agents’ B2B platforms

A survey by FICCI–EY in 2023 found 68% of passengers in Tier-2 towns preferred digital interaction for aviation services, showing latent tech readiness.

3.6. Training Pipelines and Local Manpower Pools

Instead of waiting for licensed crew, set up joint academies with FTOs in the same states — including DGCA-approved bridge programs for:

- Pilots holding CPL with only 200 hours

- Dispatcher and safety officer trainings

Similarly it should be made incumbent on the CAR 147 Type Training Organization to integrate OJT’s of trainees into one package. This should ensure that new Licensed AME’s are added to the system. The present system’s output is not commensurate with the efforts put in, and thus steps at reducing shortage of trained technical manpower in the industry are proving less effective.

Impact Example: Indonesia’s Lion Air built its own crew training program, reducing cost-per-pilot by 42% and increasing availability by 60% within 3 years.

Summary Chart: The Regional Blueprint Framework

| Pillar | Strategy Highlights | Example/Tool |

| Fleet | Standardize on supported 18–70 seaters, fuel-efficient types | ATR 42-600, Viking DHC-6 Twin Otter Series 400, Dash 8 Q 100/200/300, Embraer’s E175 |

| Airports | 40:20:40 tiered infra rollout + STOL/heliports | Modular terminals, DGCA FATO |

| Routes | Data-driven demand clusters, city-pairs with >7hr surface time | IRCTC/Ola movement analytics |

| Operations | PPP-based operator collectives, shared backend infra | CAMO, MRO, digital dispatch |

| Digital UX | Mobile ticketing, WhatsApp boarding, regional agent network | UPI/DigiYatra integrations |

| Skilling | FTO–Operator tie-ups, localized technician and flight crew upskilling | Bridge programs, CPL-to-line |

Table 3: Regional Blueprint Framework

4. Policy Recommendations & Funding Models to Supercharge Regional Connectivity

While innovative business models and operational tweaks are critical, policy innovation is the fuel that can transform potential into performance. Below are strategic recommendations for India’s aviation policymakers, DGCA, MoCA, state governments, and private stakeholders to collaboratively reshape regional aviation in Tier-2 and Tier-3 markets.

4.1. Shift from Route-Centric to Hub-Centric Incentives

UDAN has been a vital enabler, but its current structure — incentivizing specific routes — leads to fragmentation and underutilization.

Recommendation: Move toward hub-centric subsidies, where a regional base airport (e.g., Jabalpur, Jharsuguda, Belagavi) receives:

- Multi-route bidding by one operator

- Incentives based on load factor + frequency

- Infrastructure co-funding for hangars, MRO, and FTO units

Model Example: Brazil’s RAS (Regional Aviation Support) scheme funds regional hubs with pooled connectivity targets, not just individual sectors.

4.2. Create a “Regional Airline Incubation Program”

Establish a MoCA–SIDBI backed platform that supports first-time NSOP entrepreneurs with:

- Access to pre-approved lease pools of STOL aircraft

- Equity or convertible debt (₹10–15 crore) with mentoring

- Legal and CAMO support via empanelled advisors

Impact Potential: Based on industry experience, we can say that enabling merely 10 new operators in the next couple of years under such a scheme can generate 1500–3000 jobs and activate about 20 to 30 dormant / unserved airstrips across the nation.

4.3. Infrastructure Viability Gap Fund (VGF 2.0)

In addition to rute subsidies, offer infra-linked VGF for developing:

- Mini terminal buildings using prefabricated tech

- Solar-powered airfield lighting and ATC towers

- Local skill training centers for AMEs, ATCOs, and ground staff

Estimated cost per micro-regional airport upgrade: ₹20–30 crores

ROI with effective traffic management: 2.5–3.5x over 5 years

4.4. Regional Maintenance Hubs

Despite the immense efforts undertaken by the government to promote MRO activity within India, the unfortunate fact remains that still 80% in revenues accruing from this sector goes out of the country. To reduce reliance on expensive Western lessors and far-flung MROs:

- Allow tax holiday for regional MROs under ₹100 crore capex

- Extend customs duty waiver on spares/tools beyond UDAN to NSOPs operating in Tier-3

- Provide rent free gestation periods of 18 to 24 months after land allotment for organizations to develop infra before operations start.

Case in Point:

GMR Aero Technic’s expansion in Hyderabad has attracted several smaller operators to base aircraft locally, slashing ferry costs by ~28%.

4.5. Encourage State Equity Participation in Air Operators

Much like Singapore’s Temasek model or Gujarat’s investment in GIFT IFSC or taking cue from PPP models adopted for our own country to develop highways, states can:

- Pick minority equity (5–20%) in air operators serving their region

- Offer priority ATC slots, share infrastructure, help remove bottlenecks in return

- Create performance-based earn-outs linked to seat occupancy and socio-economic impact

Example: Nagaland’s past partnership with Vayudoot in the 1990s — though limited in scale — showed that joint governance improves reliability in remote areas.

Policy Strategy Matrix

| Policy Lever | Stakeholder | Outcome |

| Hub-Centric Subsidies | MoCA, State Govt | Higher load factors, better route viability |

| Incubation Program for NSOPs | MoCA, SIDBI | Lower entry barriers, skilled entrepreneurship |

| VGF for Infra | MoCA, AAI, States | Modular, sustainable airfields |

| Leasing & MRO Hubs | IFSC, DGCA, Customs | Local asset control, reduced maintenance TATs |

| State Equity Participation | State Govt, Operators | Aligned interest, long-term partnership |

Table 4: Policy Strategy Matrix

5. Final Thought: Let’s Reimagine Regional, Not Just Connect It

Let us not settle for just connecting cities—let us reimagine the aviation network to unlock prosperity for every Indian region. Regional air travel must be seen not just as transport, but as economic infrastructure—a multiplier for trade, tourism, investment, and inclusion. With vision, commitment, and collaboration, India’s regional networks are bound to flourish.

The post Reimagining Regional Aviation: Supercharging Tier-2 & Tier-3 Air Connectivity in India appeared first on N4M (News4masses).

from

https://news4masses.com/regional-aviation-supercharging-tier-2-3-air-connectivity-india/

No comments:

Post a Comment